Are you planning to buy a home or refinance your current mortgage? Understanding the current mortgage interest rates can make a big difference in how much you’ll pay each month and over the life of your loan.

These rates can change daily, affecting your budget and financial decisions. You’ll get clear, up-to-date information on today’s mortgage rates, what influences them, and how to find the best deal for your situation. Keep reading to take control of your home financing and save money where it counts.

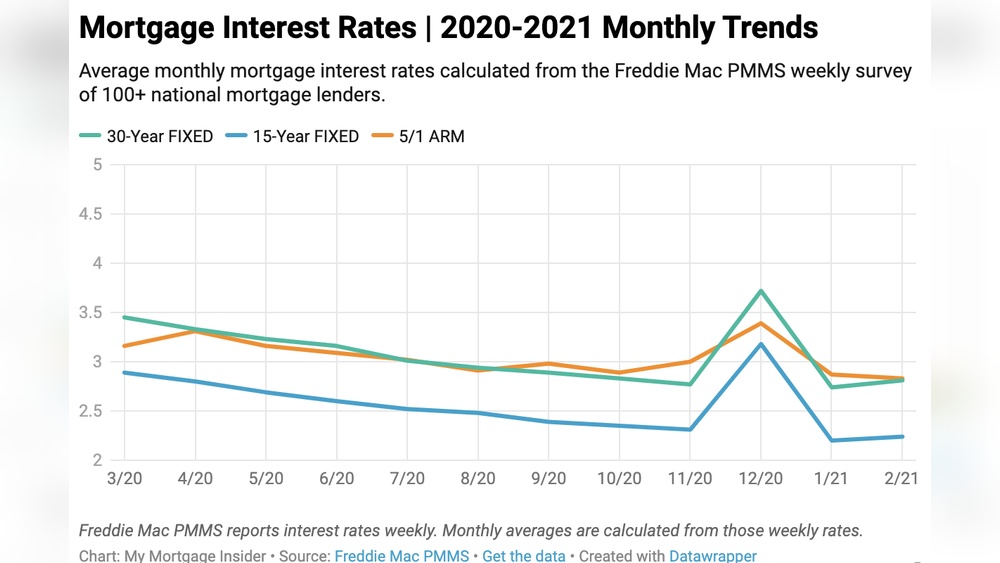

Mortgage Rate Trends

Mortgage rates have changed recently due to many reasons. Rates can go up or down each day. This affects how much people pay for a home loan.

Several factors influence mortgage rates. These include the Federal Reserve’s decisions, inflation levels, and job reports. When the economy is strong, rates might rise. When weak, rates often fall.

Economic indicators like inflation and employment numbers show the economy’s health. Higher inflation usually leads to higher rates. More jobs can mean a stronger economy and higher mortgage costs.

Types Of Mortgage Rates

Fixed-rate mortgages keep the same interest rate for the whole loan term. This means monthly payments stay steady. It is easier to plan your budget with fixed rates. These loans usually last 15 or 30 years.

Adjustable-rate mortgages (ARMs) have interest rates that change over time. The rate is low at first but can go up or down later. This means your monthly payment can vary. ARMs often start with a fixed period, like 5 years.

Hybrid mortgages combine fixed and adjustable rates. They start with a fixed rate for a set time. After that, the rate changes like an ARM. For example, a 3/1 ARM means fixed for 3 years, then adjusts yearly.

Current Rates In Austin, Texas

The average mortgage interest rate in Austin, Texas, is slightly higher than the national average. Typical rates for a 30-year fixed loan hover around 6.5%, while 15-year loans are near 5.9%. Nationally, rates tend to be about 0.2% lower, reflecting broader economic factors.

Austin’s local market affects rates due to strong housing demand and limited inventory. The city’s fast growth pushes prices up, causing lenders to adjust rates. Additionally, property taxes and home values in Austin influence mortgage costs more than in some other areas.

| Rate Type | Austin Average | National Average |

|---|---|---|

| 30-Year Fixed | 6.5% | 6.3% |

| 15-Year Fixed | 5.9% | 5.7% |

How Credit Scores Affect Rates

Credit scores play a big role in setting mortgage interest rates. Scores are grouped into tiers like excellent, good, fair, and poor. Higher tiers usually get better rates. For example, a score above 760 is considered excellent and gets the lowest rates. Scores below 620 often face higher interest rates.

Improving your credit score can lower your mortgage costs. Simple steps include paying bills on time, reducing debt, and checking your credit report for errors. These actions help raise your score over time.

| Credit Score Tier | Score Range | Typical Rate Difference |

|---|---|---|

| Excellent | 760 and above | Lowest rates |

| Good | 700 – 759 | Slightly higher than excellent |

| Fair | 620 – 699 | Moderate increase in rates |

| Poor | Below 620 | Highest rates |

Down Payment Impact

Down payment size affects mortgage interest rates significantly. A larger down payment usually means a lower interest rate. This is because lenders see less risk when borrowers invest more upfront.

Private Mortgage Insurance (PMI) is often required if the down payment is less than 20%. PMI raises the total monthly cost, even if the interest rate stays the same.

| Down Payment Size | Loan-to-Value (LTV) Ratio | Effect on Interest Rate | PMI Requirement |

|---|---|---|---|

| Less than 20% | Above 80% | Higher rates | Required |

| 20% or more | 80% or less | Lower rates | Not required |

The Loan-to-Value (LTV) ratio is the loan amount divided by the home value. A lower LTV means less risk and often a better rate. Increasing the down payment reduces the LTV ratio.

:max_bytes(150000):strip_icc()/5-16-032160ac25f043c690b2038729d4eaab.png)

Mortgage Rate Calculators

Online mortgage rate calculators help estimate monthly payments quickly. Enter the loan amount, interest rate, and loan term. The tool will show your estimated payment each month, including principal and interest.

These calculators allow easy comparison of loan options. You can change rates or terms to see which loan fits your budget best. This helps you make a clear decision before applying for a mortgage.

Using online tools saves time and avoids guesswork. They give a simple way to understand how different rates affect your loan costs. Many websites offer free calculators that update with current mortgage interest rates.

Locking In Your Rate

Locking your mortgage rate means fixing the interest rate for a set time. This protects you from rising rates during the loan process. The best time to lock is when rates are low and stable. Locking too early might miss better rates later. Locking too late risks rates going up.

| Rate Lock Period | Description |

|---|---|

| 30 Days | Common for most loans; covers the loan approval period. |

| 45 Days | Good for slower loan processes or complex deals. |

| 60 Days | Longer protection but often costs more. |

Benefits: Keeps your rate safe from increases. Helps with budgeting and planning. Risks: If rates drop, you might miss savings. Some lenders charge a fee for longer locks.

Refinancing Options

Current refinance rates often change daily. They depend on your credit score, loan type, and lender. Fixed rates give stable payments. Adjustable rates may start lower but can rise later. Comparing rates helps find the best deal.

Refinancing makes sense if new rates are lower than your current rate. It can reduce monthly payments or loan term. Also consider your financial goals, such as paying off faster or lowering costs.

| Costs | Savings |

|---|---|

| Application fees | Lower monthly payments |

| Appraisal fees | Reduced interest over time |

| Closing costs | Shorter loan term options |

| Prepayment penalties | Improved cash flow |

Calculate total costs versus savings to decide wisely. Refinancing can save money if savings exceed costs.

Future Rate Predictions

Experts predict mortgage rates will change in the near future. Many expect rates to rise slowly due to inflation pressures. Others believe rates might stay steady if the economy weakens. Watching key economic factors can help understand these changes. Inflation, employment rates, and central bank policies all play a big role.

Preparing for future rates means considering your budget carefully. Locking in a rate now might save money later if rates climb. Refinancing could also be an option if rates drop. Staying informed about economic news and rate updates is important.

Frequently Asked Questions

What Is A 30-year Mortgage Rate Right Now?

The current 30-year mortgage rate in the U. S. averages around 6. 5%. Rates vary by lender and location. Check daily updates for precise rates.

How To Get A 4% Interest Rate On A Mortgage?

Improve your credit score, increase your down payment, choose a shorter loan term, and shop lenders. Lock rates during low-rate periods.

Will Mortgage Rates Be 3% Again?

Mortgage rates may not return to 3% soon due to economic factors and inflation. Rates depend on market conditions. Stay updated for changes.

How Much Is A $500,000 Mortgage At 6% Interest?

A $500,000 mortgage at 6% interest typically costs about $3,000 monthly. This assumes a 30-year fixed loan term. Exact payments vary by loan type and term. Use a mortgage calculator for precise figures.

Conclusion

Mortgage interest rates change often. Staying informed helps you make smart choices. Check rates regularly to find the best deal. Remember, small differences affect your monthly payment. Understanding current rates saves you money over time. Keep an eye on market trends and news.

Speak with a lender to get personalized advice. Taking action now can improve your home loan terms. Stay patient and ready for the right opportunity.

Read More

- 30 Year Fixed Mortgage Rates: What You Need to Know Now

- Buy to Let Mortgage Rates UK: Unlock Best Deals Today

- Jumbo Mortgage Rates Today: Unlock Low Rates & Save Big

- Lowest Refinance Mortgage Rates: Unlock Big Savings Today!

- Best Refinance Lenders Online: Top Picks for Low Rates Today

- Cash Out Refinance Rates: Unlock Savings with Top Tips

- Home Refinance Savings Calculator: Maximize Your Mortgage Savings Today

- Mortgage Refinance Closing Costs: What You Need to Know Today

- Va Home Loan Interest Rates: Unlock Best Deals Today

- Fha Mortgage Loan Rates: Unlock Today’s Best Deals Now