Thinking about refinancing your home loan but unsure if it’s worth the effort? You’re not alone.

Refinancing can save you a significant amount of money each month, but the numbers can be confusing. That’s where a Home Refinance Savings Calculator becomes your best friend. This simple tool puts the power in your hands by showing exactly how much you could save by refinancing your mortgage.

Imagine knowing upfront how much extra cash you’ll have every month or how quickly you could pay off your home. Keep reading to discover how this calculator works and how it can help you make smarter financial decisions for your future.

How Refinancing Works

Mortgage means a loan to buy a house. It has terms like principal (the amount you borrow), interest rate (the cost of borrowing), and term (the time to pay back). Monthly payment includes principal plus interest and often taxes.

Refinancing means replacing your old loan with a new one. People refinance to get a lower interest rate, reduce monthly payments, or change loan length. It can also help switch from an adjustable rate to a fixed rate.

Consider refinancing when interest rates drop, your credit improves, or your financial goals change. Also, when you plan to stay in your home long enough to cover refinancing costs, it may save money.

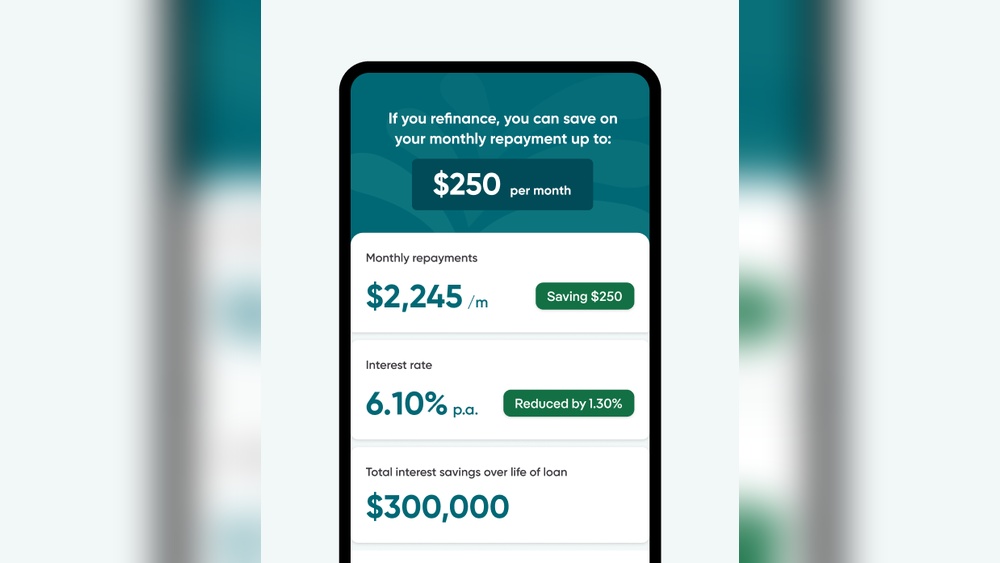

Calculating Savings

The key inputs for the refinance savings calculator include your current loan balance, interest rate, and loan term. You must also enter the new loan details like the proposed interest rate and term length. These details help compare costs and savings accurately.

Monthly payment comparison shows how much you pay now versus after refinancing. Lower monthly payments can free up cash for other expenses. The calculator breaks down principal and interest amounts for easy understanding.

The interest rate impact is significant. Even a small rate drop can save thousands over time. The calculator estimates total interest paid and highlights savings. It helps decide if refinancing is worth the cost.

Types Of Refinance Options

Rate-and-term refinance changes the interest rate or loan length. It helps lower monthly payments or pay off the loan faster. This option does not add extra cash to the loan balance.

Cash-out refinance lets homeowners borrow more than they owe. They get the difference in cash. This is useful for paying off debt or home improvements.

Streamline refinance is faster and easier. It requires less paperwork and no home appraisal. It is available for certain government-backed loans, like FHA or VA loans.

Fees And Costs To Consider

Closing costs usually include fees like appraisal, title insurance, and loan origination. These can add up to 2-5% of your loan amount. It is important to know these costs before refinancing.

Prepayment penalties may apply if your current loan charges fees for paying off early. These penalties vary and can cost a few hundred to several thousand dollars.

Hidden charges might include document fees, courier fees, or underwriting fees. These small fees can surprise you if not checked carefully.

| Fee Type | Description | Typical Cost |

|---|---|---|

| Appraisal Fee | Cost to value your home | $300 – $700 |

| Title Insurance | Protects lender and owner | $500 – $1,000 |

| Loan Origination Fee | Charged by lender to process loan | 0.5% – 1% of loan |

| Prepayment Penalty | Fee for early loan payoff | Varies |

| Other Fees | Document, courier, underwriting fees | $100 – $500 |

Using The Refinance Savings Calculator

Enter your current loan details into the calculator. Add your new loan terms like interest rate and loan length. Press calculate to see your potential savings. The tool shows monthly payment differences and total interest saved over time.

Look closely at the monthly savings and total cost reduction. Check how long it takes to recover closing costs from these savings. Compare your current mortgage details with the new loan offer carefully. Use these numbers to decide if refinancing is worth it.

Avoid common mistakes like entering wrong loan amounts or interest rates. Do not forget to include closing costs in your calculations. Avoid ignoring the loan term changes; they affect your total savings. Double-check all inputs before trusting the results.

Maximizing Your Savings

Improving your credit score can lower your refinance interest rates. Paying bills on time and reducing debt helps. Check your credit report for errors. Fix any mistakes quickly. A higher credit score means better loan offers and lower monthly payments.

Choosing the right loan term affects your savings. Shorter terms have higher payments but save money on interest. Longer terms lower monthly payments but cost more overall. Pick a term that fits your budget and goals.

Negotiating better rates can reduce your costs. Shop around and compare offers from different lenders. Ask if they can lower fees or interest rates. Even a small rate drop can save thousands over time.

Break-even Analysis

The break-even point shows when savings from refinancing cover the costs. To find it, divide the total refinance costs by the monthly savings gained.

For example, if refinancing costs $3,000 and saves $200 per month, the break-even point is 15 months. This means after 15 months, you start saving money.

Use this point to decide if refinancing makes sense. If you plan to stay in your home longer than the break-even time, refinancing may save you money.

Refinancing only helps if the monthly savings are higher than the new monthly costs. Always compare the old and new loan terms carefully.

Impact On Your Financial Goals

Lowering monthly payments can free up cash for other needs. Refinancing often reduces your interest rate, which means smaller monthly bills. This helps you manage your budget better and avoid stress.

Building home equity faster is another benefit. By refinancing to a shorter loan term, more of your payment goes toward the principal. This grows your home’s value quicker and increases your net worth.

Funding other expenses is possible by using cash-out refinancing. You can borrow against your home’s equity to pay for things like home repairs, education, or emergencies. This option offers flexibility without high-interest credit cards.

Local Considerations For Austin, Texas

Austin’s housing market shows steady growth with rising home values. Interest rates have stayed relatively low, making refinancing attractive for many homeowners. This trend can help you save on monthly mortgage payments.

State and local incentives may also affect refinancing costs. Texas offers certain property tax benefits and programs that support homeowners. Checking for these incentives can increase your savings and lower expenses.

Choosing lenders local to Austin provides benefits like better customer service and quicker processing. Local lenders understand Austin’s market and can offer competitive rates and tailored loan options. Comparing several lenders helps find the best terms for your refinance.

Frequently Asked Questions

What Is The 2% Rule For Refinancing?

The 2% rule for refinancing means your new loan must reduce your monthly payment by at least 2% to justify costs.

Is It Worth Refinancing To Save 2%?

Refinancing to save 2% can be worth it if savings exceed closing costs and you plan to stay long-term. Use a refinance calculator to compare costs and benefits before deciding.

What Is The 80/20 Rule In Refinancing?

The 80/20 rule in refinancing means financing 80% of your home’s value with a first mortgage and 20% with a second loan.

How Much Does It Cost To Refinance A $400,000 Home?

Refinancing a $400,000 home typically costs 2% to 5% of the loan amount. Expect $8,000 to $20,000 in fees.

Conclusion

Using a home refinance savings calculator helps you see clear benefits. It shows potential monthly savings and overall costs. This tool makes comparing your current loan simple and fast. Knowing your savings helps you decide if refinancing fits your goals.

Always check multiple scenarios to find the best option. Smart choices today can lead to better financial health tomorrow. Keep your budget in mind and use the calculator often. Refinancing might save you money and reduce your stress.