Thinking about refinancing your mortgage? One important factor you can’t overlook is the closing costs involved.

These fees can catch you by surprise if you’re not prepared. But what exactly are mortgage refinance closing costs, how much will you pay, and are there ways to reduce or even avoid them? Understanding these details can save you money and help you decide if refinancing makes sense for your situation.

Keep reading to uncover the key facts about closing costs, common fees you might face, and smart strategies to manage them—so you can make confident choices about your mortgage refinance.

Refinance Closing Costs

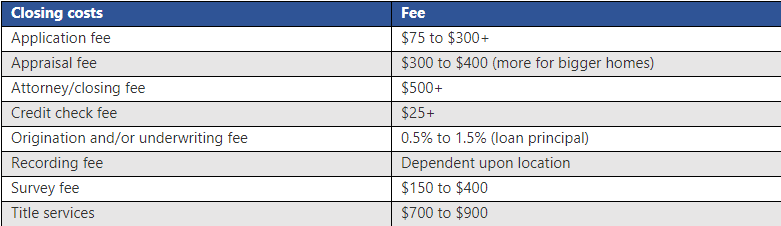

Refinance closing costs include several common fees. These fees cover processing, appraisal, and credit checks. Expect to pay loan origination fees and sometimes points to lower your interest rate. Title search and title insurance protect ownership rights and are often required.

Costs differ by state and loan type. Some states have higher taxes or special fees. Loan size also affects the cost. Larger loans usually have higher fees.

| Fee Type | Purpose | Typical Cost |

|---|---|---|

| Loan Origination Fee | Processing the loan application | 0.5% – 1% of loan amount |

| Appraisal Fee | Estimate home value | $300 – $500 |

| Title Search | Verify property ownership | $200 – $400 |

| Title Insurance | Protect against ownership issues | $500 – $1,000 |

Ways To Reduce Closing Costs

Lender fee waivers can lower your refinance closing costs. Some lenders may reduce or remove fees like application or processing charges. It never hurts to ask your lender about available waivers.

Shopping for service providers allows you to find better prices. You can choose your own title company, home inspector, or attorney. Comparing multiple providers helps you pick the lowest-cost option.

Negotiating closing fees with your lender or service providers might save money. Some fees are flexible, such as administrative or courier charges. Politely requesting a discount or waiver can reduce your total closing costs.

Paying Closing Costs

Paying closing costs can be done in different ways. One option is to pay out-of-pocket at closing. This means you bring the money to the table and pay the fees upfront. These costs include fees for appraisal, title, and loan processing.

Another way is rolling the costs into the loan. This adds the closing costs to your new loan amount. Your monthly payments will be a bit higher, but no cash is needed right away.

There are also no-closing-cost refinance options. The lender pays the fees, but you get a slightly higher interest rate. This choice helps avoid upfront payments but can cost more in the long run.

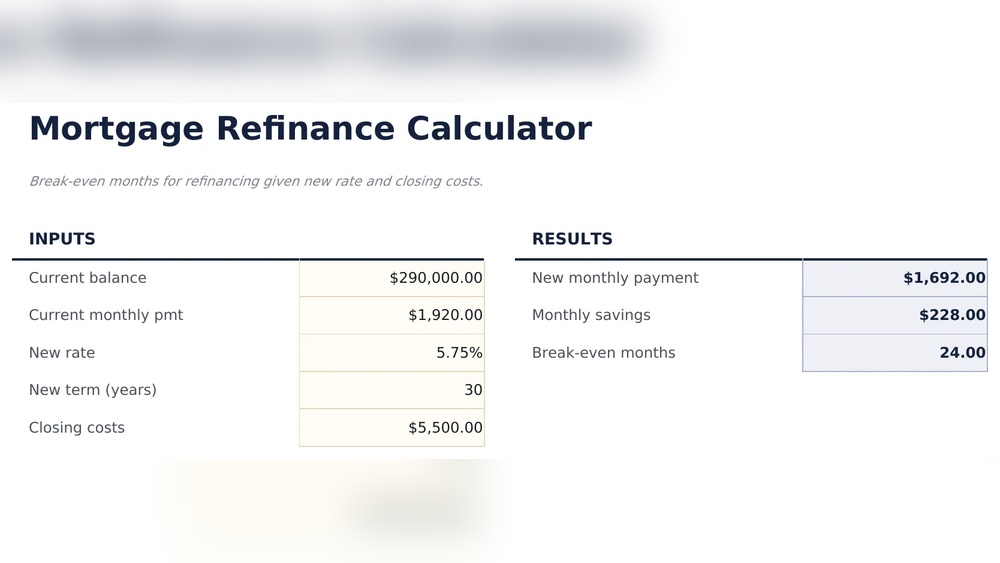

Calculating Savings And Break-even

Refinance calculators help estimate monthly payments after refinancing. Enter your loan amount, interest rate, and term to see changes.

These tools show how much you might save each month. They also factor in closing costs that come with refinancing.

The break-even point tells when savings cover these costs. It is the time needed to recover your closing expenses.

Calculate break-even by dividing closing costs by monthly savings. For example, if costs are $3,000 and you save $150 monthly, break-even is 20 months.

Knowing this helps decide if refinancing is worth it. Use multiple calculators to compare results and make an informed choice.

When To Refinance

Refinancing can save money, but closing costs matter a lot. Compare the costs of refinancing with the savings in monthly payments to decide.

Lower interest rates reduce monthly payments. Even a small drop can help, but be sure to check if the savings cover the closing costs.

Changing the loan term affects payments too. Shorter terms mean higher payments but less interest overall. Longer terms lower payments but can increase total interest.

Legal And Recording Fees

Recording fees cover the cost to register your new mortgage with the local government. This step makes the loan official and public. The fees vary by location but are usually a small part of your closing costs.

Typically, the borrower pays the recording fees. Sometimes the lender or seller may cover part of it, depending on the agreement. Clarifying who pays these fees before closing helps avoid surprises.

Recording fees add to the total closing costs. Though small, they are important for finalizing the refinance process. Budgeting for these fees ensures smoother closing and no last-minute issues.

Frequently Asked Questions

Are There Closing Costs For Refinancing A Mortgage?

Yes, refinancing a mortgage involves closing costs like appraisal, title, and origination fees. Costs vary by lender and location. Some lenders may offer no-closing-cost refinancing by increasing the interest rate. You can also roll closing costs into the new loan balance to avoid upfront payments.

What Is The 2% Rule For Refinancing?

The 2% rule for refinancing means your closing costs should be about 2% of your loan amount. It helps estimate refinancing expenses quickly.

How Much Does It Cost To Refinance A $400,000 Home?

Refinancing a $400,000 home typically costs 2% to 5% of the loan amount. Expect $8,000 to $20,000 in fees. Costs include appraisal, title, and lender fees. Some lenders offer no-closing-cost refinancing by increasing your interest rate. Always compare offers to minimize expenses.

Does Refinancing Include Closing Costs?

Yes, refinancing usually involves closing costs like appraisal, title, and loan fees. You can roll these costs into your loan or pay them upfront. Some lenders offer no-closing-cost refinancing by charging a higher interest rate instead.

Conclusion

Refinancing a mortgage involves various closing costs. These costs can vary by lender and location. Understanding each fee helps avoid surprises at closing. You might negotiate some fees or shop around for better prices. Rolling costs into your loan increases monthly payments but reduces upfront cash needs.

A no-closing-cost refinance may raise your interest rate slightly. Use online calculators to estimate your savings and break-even point. Careful planning ensures refinancing makes financial sense for you. Stay informed and choose options that fit your budget best.

Read More

- Current Mortgage Interest Rates: What Homebuyers Need to Know Today

- 30 Year Fixed Mortgage Rates: What You Need to Know Now

- Buy to Let Mortgage Rates UK: Unlock Best Deals Today

- Jumbo Mortgage Rates Today: Unlock Low Rates & Save Big

- Lowest Refinance Mortgage Rates: Unlock Big Savings Today!

- Best Refinance Lenders Online: Top Picks for Low Rates Today

- Cash Out Refinance Rates: Unlock Savings with Top Tips

- Home Refinance Savings Calculator: Maximize Your Mortgage Savings Today

- Va Home Loan Interest Rates: Unlock Best Deals Today

- Fha Mortgage Loan Rates: Unlock Today’s Best Deals Now