Thinking about investing in property with a buy-to-let mortgage in the UK? Understanding the current mortgage rates can make a huge difference to your returns.

Whether you’re a seasoned landlord or just starting out, knowing how these rates work and where to find the best deals is essential for maximizing your profit. You’ll discover clear insights into buy-to-let mortgage rates, key factors that affect them, and smart tips to help you secure the right mortgage for your investment goals.

Keep reading to make sure your buy-to-let venture sets off on the right foot and stays profitable.

Current Buy To Let Rates

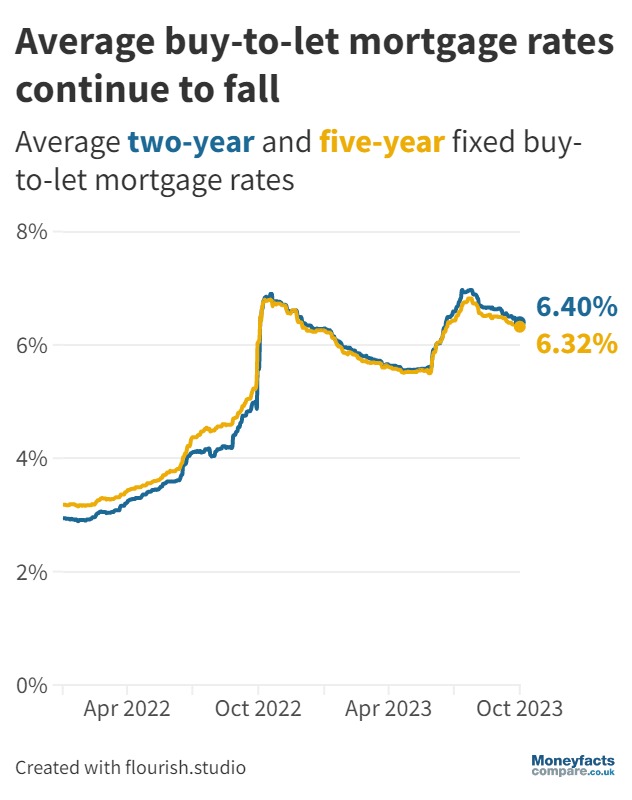

Buy to let mortgage rates in the UK depend on the loan-to-value (LTV). Typically, the higher the LTV, the higher the interest rate. For example, a 60% LTV might have an average two-year fixed rate of around 4%, while an 80% LTV could be closer to 5%. Rates change often, so checking current offers helps.

| Maximum Loan-To-Value (LTV) | Average Two-Year Fixed Rate | Average Five-Year Fixed Rate |

|---|---|---|

| 60% | 4.0% | 4.5% |

| 75% | 4.5% | 5.0% |

| 80% | 5.0% | 5.5% |

Top lenders offer various deals to suit different needs. Fixed rates give certainty by keeping payments stable for a set time. Variable rates may start lower but can change, affecting monthly costs. Choosing depends on personal comfort with risk and how long you plan to keep the property.

Finding Best Deals

Using comparison platforms like MoneySuperMarket or Moneyfacts helps find the best buy-to-let mortgage rates. These sites show live deals from many lenders quickly. You can compare rates based on your deposit and loan needs.

Specialist lenders often offer tailored deals for landlords and may accept complex income types. High street lenders usually have stricter rules but are easier to work with. Both have pros and cons to consider.

| Type | Advantages | Disadvantages |

|---|---|---|

| Specialist Lenders | More flexible criteria, good for complex cases | Higher rates, less known brands |

| High Street Lenders | Lower rates, trusted brands | Stricter lending rules |

Limited company mortgages are for landlords who buy property through a company. They may offer tax benefits and different rates. Some lenders specialize in these, so comparison is key.

Deposit Requirements

Typical deposit amounts for buy-to-let mortgages usually start at 25% of the property value. Some lenders may ask for a higher deposit, especially for high value mortgages. These mortgages often require deposits of 30% or more, depending on the lender’s criteria.

For first-time landlords, some lenders offer special deals but still expect a minimum deposit of 25%. Proof of rental income potential and credit history are important factors. Lenders want to see stable finances before approving any mortgage.

| Type | Typical Deposit | Notes |

|---|---|---|

| Standard Buy-to-Let | 25% | Most common deposit requirement |

| High Value Mortgages | 30% or more | For properties above standard lending limits |

| First-Time Landlords | 25% | May require proof of rental income |

Rental Income And Affordability

Interest Coverage Ratio (ICR) measures if rental income covers mortgage payments. Lenders usually require rent to be 125% of mortgage interest. This protects against income drops or rate rises. Stress testing simulates higher interest rates to ensure affordability. It shows if rent still covers payments when rates rise.

Rental income is taxed, affecting profitability. Landlords must declare rental profits on tax returns. Allowable expenses reduce taxable income. These include mortgage interest, repairs, and letting agent fees. Higher rental income can push landlords into a higher tax bracket.

| Factor | Details |

|---|---|

| Interest Coverage Ratio | Minimum 125% rent cover over mortgage interest |

| Stress Testing | Checks affordability with higher interest rates |

| Tax Implications | Rental profits taxed after allowable expenses |

Mortgage Application Tips

Mortgage brokers help find the best buy-to-let mortgage rates. They compare many lenders quickly. Brokers know the market and can explain terms clearly. Using a broker can save time and money. They also help with tricky paperwork.

Essential documents for mortgage applications include proof of income, bank statements, and ID. Landlords often need rental income details too. Having all papers ready speeds up the process. Missing documents can cause delays or rejection.

Common pitfalls include not checking all fees, ignoring credit score impact, and underestimating costs. Some buyers forget to factor in taxes and maintenance. Avoid rushing and read all terms carefully. Asking questions can prevent mistakes.

Landlord Considerations

Tax brackets can affect how much tax landlords pay on rental income. Rental income adds to total earnings and might push landlords into a higher tax rate. This reduces the profit from rent. Landlords should track their income to avoid unexpected tax bills.

Managing multiple properties means handling more tenants, maintenance, and administration. It requires good organization and time management. Each property might have different legal rules and needs, so landlords must stay informed to avoid fines.

Legal responsibilities include ensuring safe living conditions and following rental laws. Landlords must provide necessary certificates, like gas safety and energy performance. They should also understand eviction rules and tenant rights to stay compliant and protect their investment.

Frequently Asked Questions

Can A 70 Year Old Woman Get A 30 Year Mortgage?

Yes, a 70-year-old woman can get a 30-year mortgage. Approval depends on lender policies and income stability.

Is It Still Worth Doing Buy-to-let In The Uk?

Buy-to-let in the UK can still be profitable with careful tax planning and choosing the right property. Monitor rental income and mortgage rates closely.

What Is The 3 7 3 Rule?

The 3 7 3 rule guides email writing: 3 lines for greeting, 7 lines for the message, 3 lines for closing.

What Are Current Buy-to-let Mortgage Rates In The Uk?

Buy-to-let mortgage rates in the UK vary but typically range between 3% and 5%. Rates depend on loan-to-value ratio, lender, and property type. Fixed-rate deals are popular for stability and often last 2 to 5 years.

Conclusion

Buy to let mortgage rates in the UK change often. Watching rates helps landlords save money. Choose a mortgage that fits your budget and goals. Comparing deals makes finding the best rate easier. Understand your rental income and tax duties well.

Smart choices lead to steady rental profits. Keep learning about the market for success.